I. From spot to the bigger market

Part I of this series argued that crypto liquidity concentrates by design. The gravity pulling volume into a handful of assets, Bitcoin, Ethereum, and a thin tier of alternatives, was rational market structure, not a sign of immaturity. The argument focused on spot.

The harder question is what happens when spot stops being the relevant market.

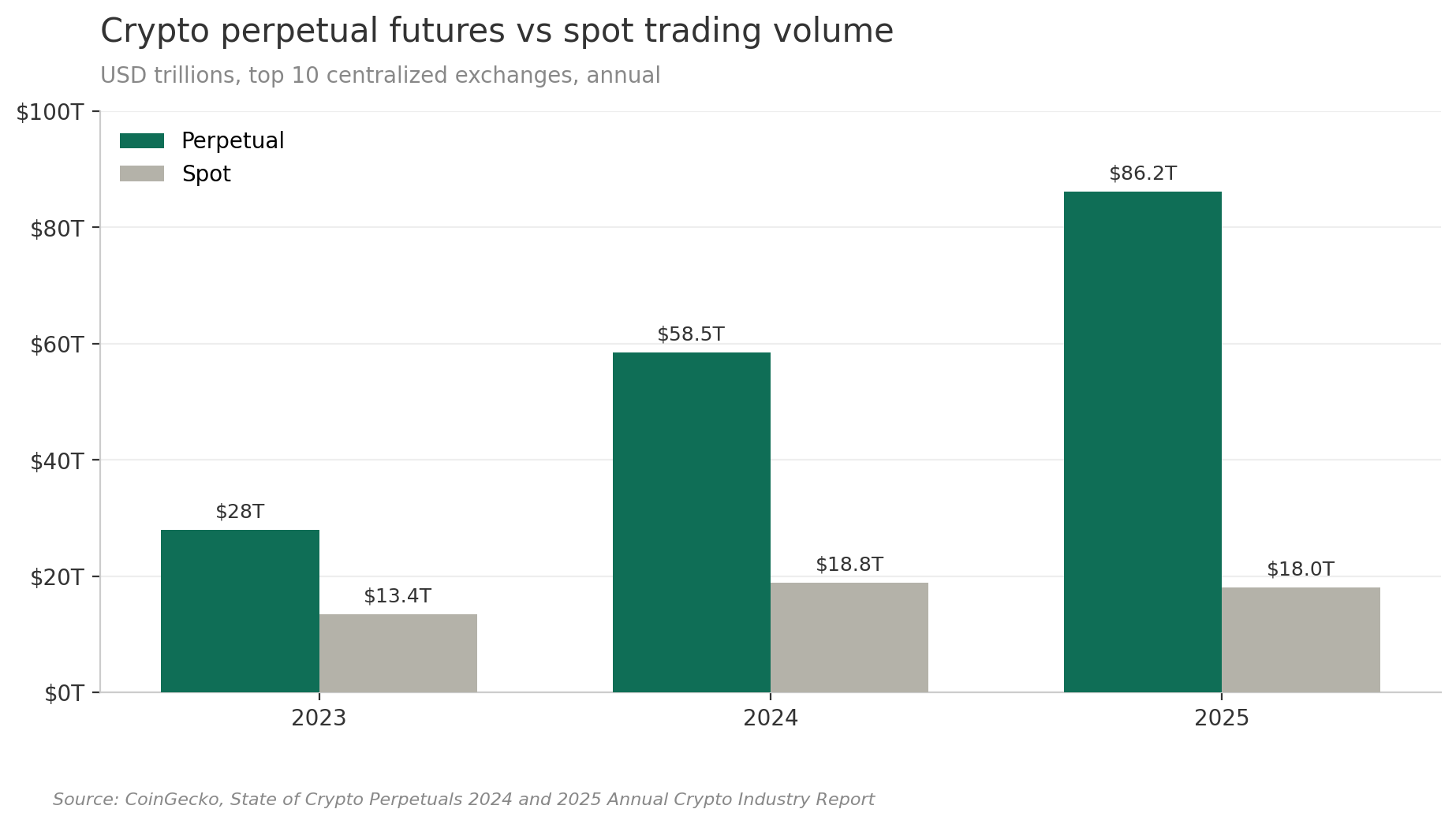

In 2025, perpetual futures volume on top centralized crypto exchanges reached $86T, against approximately $18T in spot trading. By Q1 2026, the ratio of derivatives to spot reached roughly 5:1. Perpetuals now represent the majority of all crypto trading volume.1 Price discovery, leverage, and risk transfer happen on perpetual markets. Spot is the settlement layer.

This piece picks up where Part I left off: if liquidity concentrates within an asset, why does it fragment so violently across venues, and what happens when that pattern gets exported to every other asset class?

II. The market that beat spot

Traditional futures expire. That single design choice creates contract rolls, calendar spreads, basis convergence, and constant operational overhead. The perpetual future, popularized by BitMEX in 2016, removed expiry entirely. A funding rate mechanism, with payments transferred between longs and shorts every 8 hours, pulls the perpetual price toward spot. Once the format existed, the operational cost of holding leveraged crypto exposure collapsed.

The format also enabled leverage at scale traditional clearinghouses cannot offer, with 50x to 125x routinely available and up to 500x on some venues.2 This is only possible because of two structural innovations: auto-deleveraging, which closes profitable opposing positions when liquidations cannot clear, and socialized losses, which distribute shortfalls across remaining traders. These shift counterparty risk in ways traditional futures explicitly designed against, but they make extreme leverage operationally viable.

Annual perpetual volume on top centralized exchanges reached $28T in 2023, $58.5T in 2024, and $86.2T in 2025.3 Spot volume stayed roughly flat across the same period. The ratio inverted.

Annual perpetual futures volume on top centralized exchanges in 2025, more than triple the $28T traded in 2023. Spot volume stayed roughly flat at $18T. Perpetuals are no longer a hedging instrument bolted onto spot markets, they are the primary venue for price discovery and risk transfer in digital assets.

The structural consequence is that perpetuals created complete markets in crypto. Long and short expression became symmetric for any token with a contract. Shorting a single name, operationally cumbersome in equities and effectively impossible in many commodities, became trivial. Price discovery shifted from spot to derivatives, and stayed there.

For institutions, this is the part of crypto market structure that translates most directly. The expiry problem exists in every asset class. The format that solved it for crypto is now being applied elsewhere.

III. Other assets are arriving on the rails

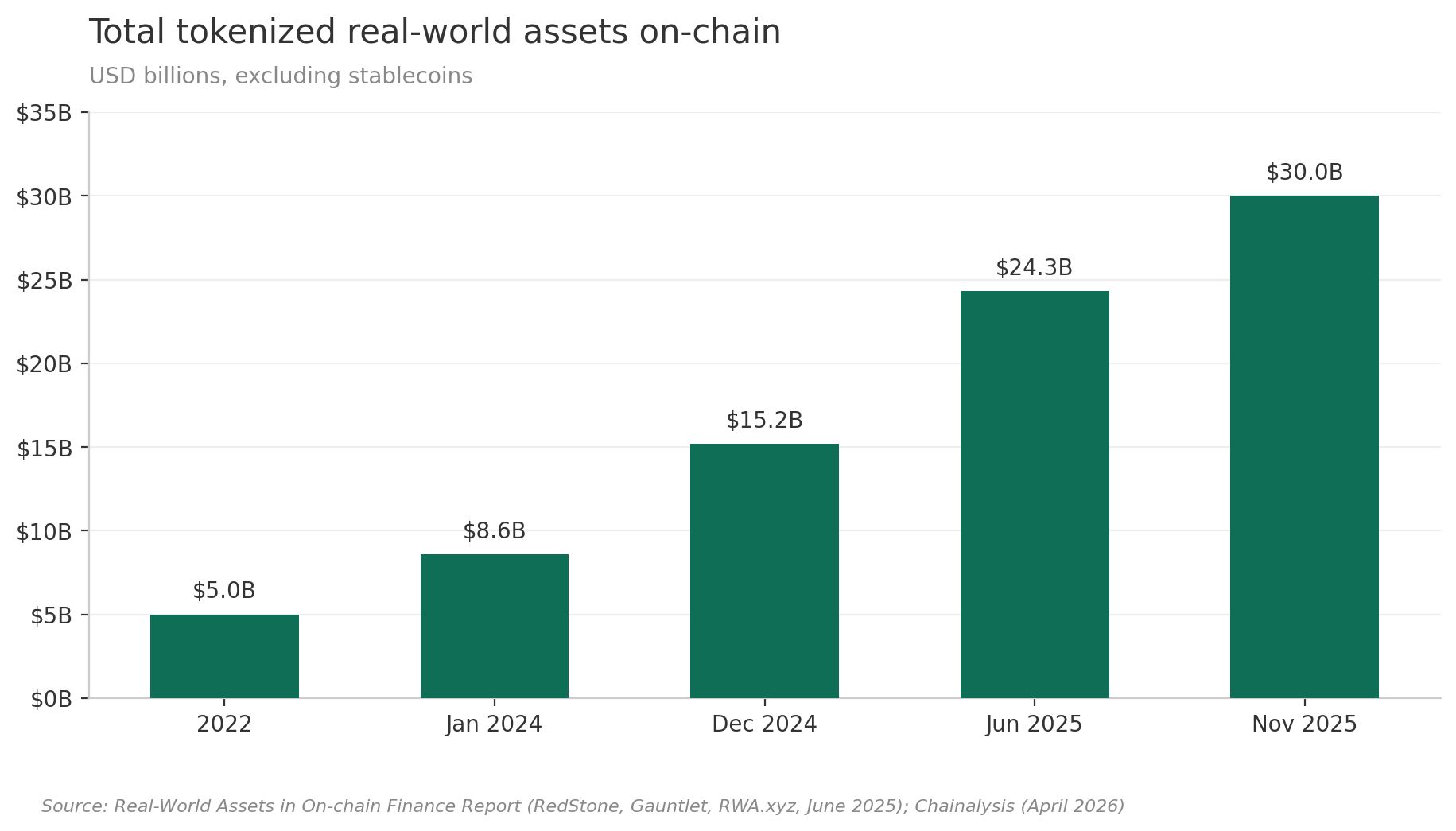

Tokenized real-world assets on-chain (excluding stablecoins) grew from roughly $5B in 2022 to nearly $30B by November 2025. Tokenized US Treasuries alone expanded from approximately $100M in January 2023 to over $15B by April 2026, a 150x increase in three years. BlackRock’s BUIDL fund alone holds nearly $3B in tokenized short-term Treasuries.4

Total tokenized real-world assets on-chain by November 2025, up from approximately $5B in 2022. Tokenized US Treasuries alone grew from $100M to over $15B in three years. The institutional adoption of crypto’s structural properties is no longer theoretical, it is being deliberately engineered into other asset classes at scale.

The tokenization is happening. The more interesting development is what is being built on top of it.

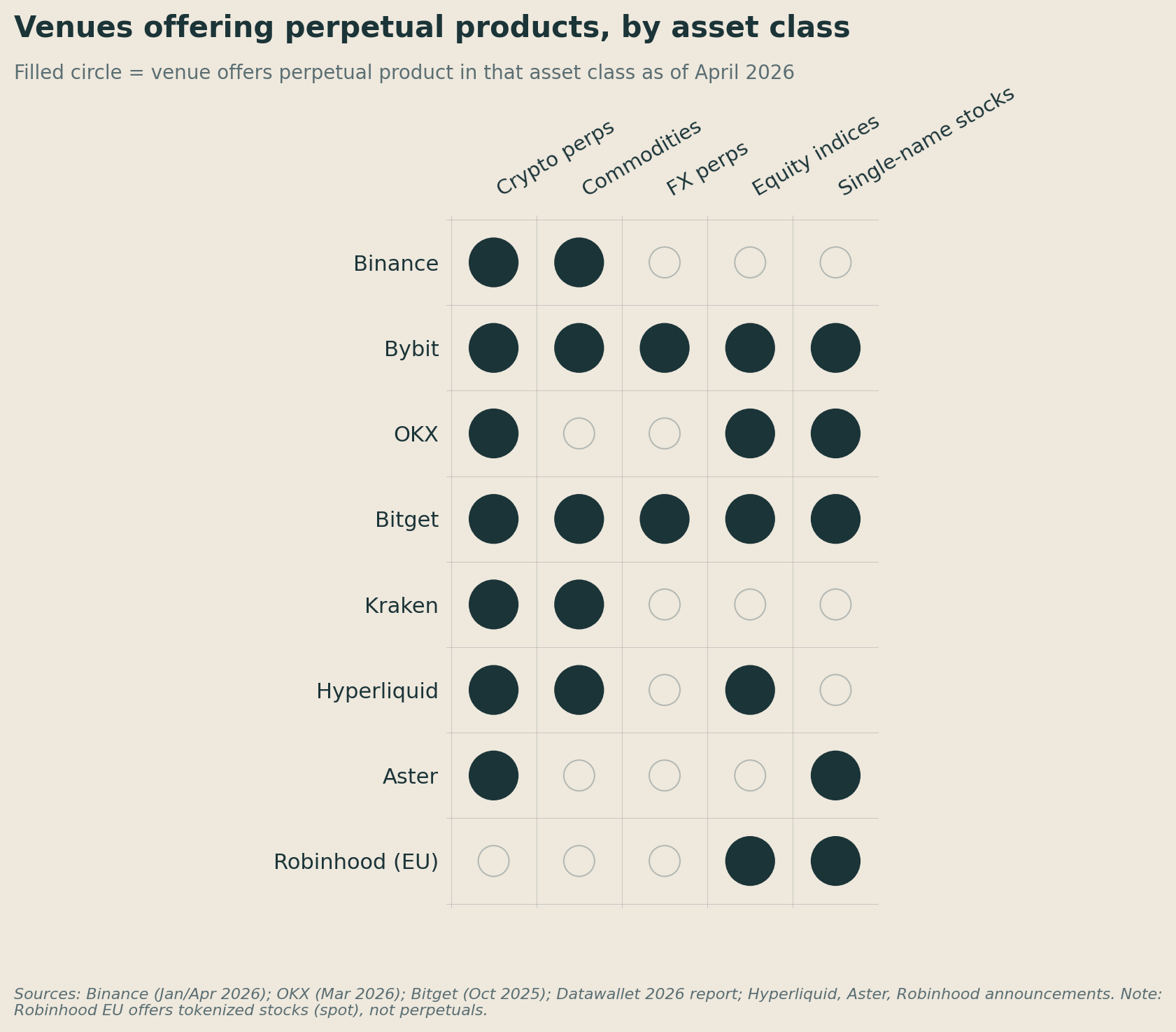

The pace of expansion has accelerated. Hyperliquid, which launched in late 2023 as an on-chain perpetual futures exchange, now lists perpetuals on gold, silver, and oil. On a single day in January 2026, it accounted for 2% of global daily silver trading volume on a contract that had been live for less than a month.5 Binance followed in January 2026 with regulated gold and silver perpetuals, then expanded to oil and natural gas in April 2026.6 OKX launched single-stock perpetuals in March 2026 covering NVDA, AAPL, MSFT, GOOGL, META, and others, plus index trackers QQQ and SPY.7 Bitget added US stock index perpetuals in October 2025. Bybit now offers products spanning crypto, gold, FX, equities, and single-name stocks. Robinhood launched tokenized US stocks and ETFs on Arbitrum for European users in summer 2025.8 Aster offers 24-hour stock perpetuals with extreme leverage.

The center of gravity for new trading formats is no longer in Chicago or New York. It is in venues that did not exist five years ago, expanding outward from crypto into every asset class that can be tokenized.

IV. Why crypto’s format is pulling everything in

The question is why this is happening at this speed. The answer is that crypto built four infrastructure properties that no other major asset class combined before, and a derivatives format that solved problems traditional futures could not.

The infrastructure properties came almost by accident. A bitcoin in Singapore is identical to a bitcoin in New York: no jurisdictional wrappers, no corporate actions, no settlement cycle differences. The market is open every hour because the network produces blocks every hour. Settlement happens on-chain in seconds, with the participant holding the asset rather than a custodian. Removing the custodian as a structural intermediary was the most consequential of the four. T+2 settlement and tri-party custody arrangements existed because the alternative was not technically possible at scale. Until it was.

These are not crypto-specific properties. They are infrastructure properties. Once the rails existed, every asset class had a question to answer: do we want to inherit this. Tokenized Treasuries, tokenized equities, commodity perpetuals, and on-chain credit are the answer.

The perpetual format itself is the second piece. This is not the first time someone tried to build a market for leveraged single-name exposure. Single-stock futures launched on the NSE in 2001 and briefly made India the world’s largest SSF venue, but they had fallen to roughly 12% of Indian equity derivatives by the mid-2010s, displaced by index options.9 In the US, SSFs never developed at all, displaced by the depth of the listed options market and the operational ease of stock borrows for institutions who needed short exposure. The format failed.

Perpetuals on single tokens addressed the same need with a different format and succeeded at scale. The lesson is that the format is what matters. And the format is now being applied to every asset class that the new infrastructure rails can support.

This is convergence: not the convergence of asset classes, but the convergence of trading format. Every asset class moving onto these rails inherits the same infrastructure, the same derivatives format, and as we will see, the same fragmentation.

V. The new fragmentation

The intuitive expectation when markets converge is that liquidity consolidates. Trading formats become standardized, and a small number of dominant platforms emerge, the way three exchanges came to dominate US equities, or CME effectively owns global futures benchmarks.

The convergence underway in crypto-native markets is doing the opposite. It is fragmenting.

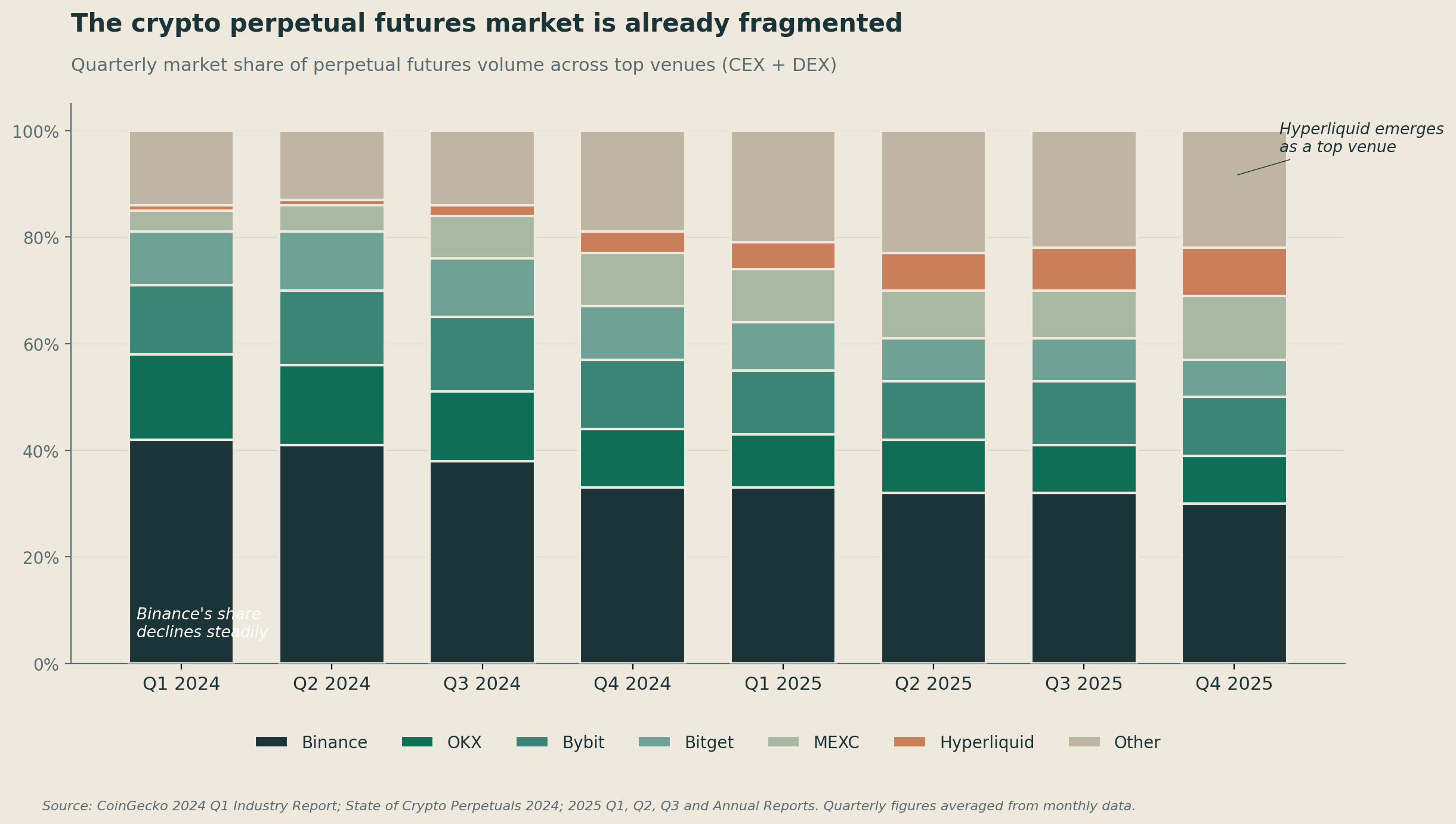

The number of perpetual contracts that are fungible across major venues. A BTC perp on Binance is not the same instrument as a BTC perp on Hyperliquid. Different funding mechanics, different risk engines, different liquidity profiles. Spot bitcoin is fungible. Bitcoin perps are not. This is the opposite of how traditional futures work, where a CME E-mini is a CME E-mini regardless of who routes the trade, and it has direct consequences for how liquidity will distribute across the converged market.

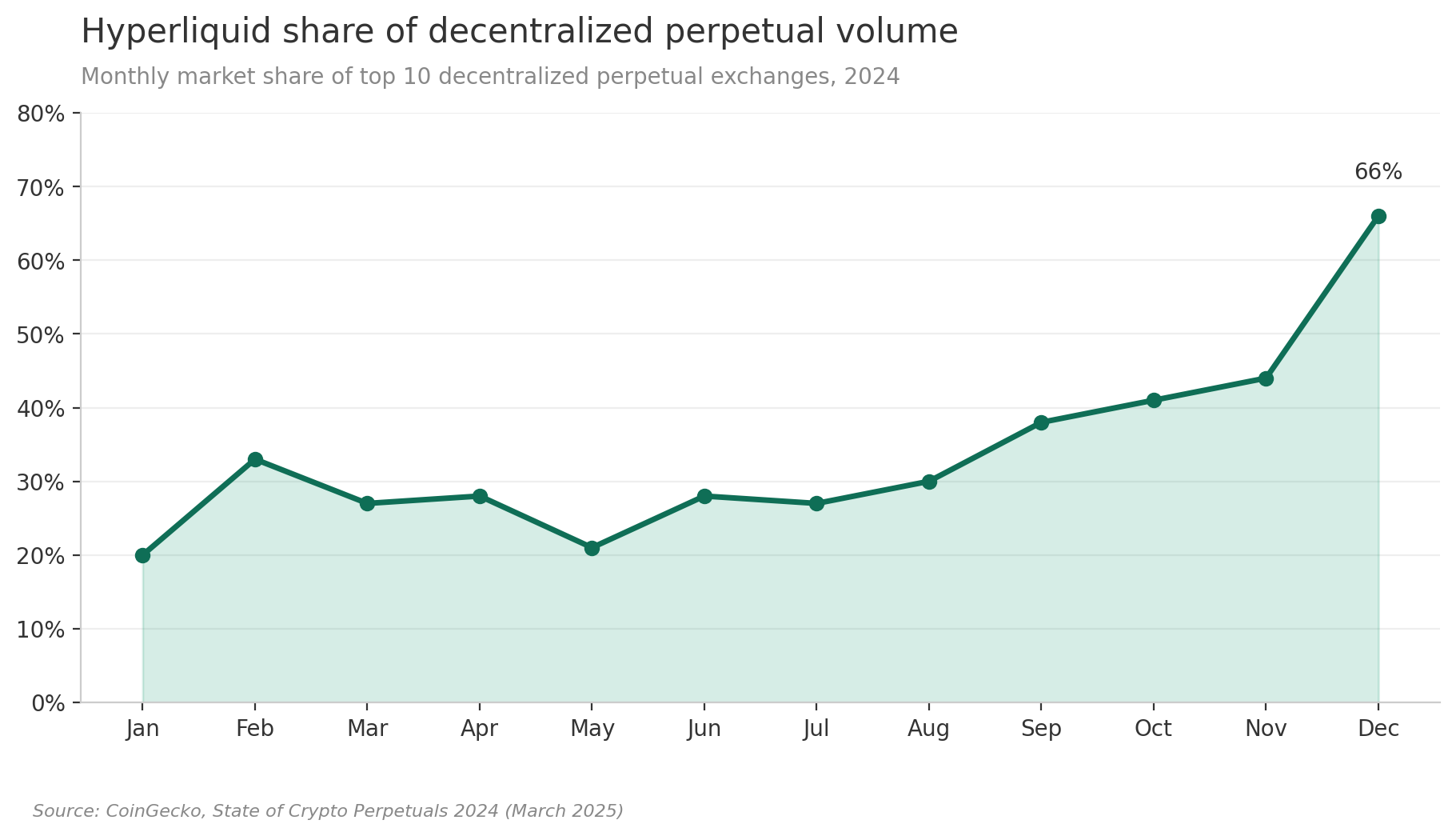

The data shows fragmentation accelerating, not resolving. Binance’s share of CEX perpetual volume fell from 43% at the start of 2024 to roughly 30% by end of 2025, even as the overall market more than doubled.10 No single venue holds more than a third of total perpetual volume. Hyperliquid emerged from negligible share in early 2024 to roughly 9% of the total market by late 2025, almost entirely on the back of decentralized infrastructure and a token airdrop.

The fragmentation has multiple layers. CEX perps trade against CEX perps; DEX perps trade against DEX perps; cross-margining between the two is rare. Hyperliquid liquidity is not Binance liquidity, and the structural divide between centralized and decentralized venues is itself a fragmentation axis that traditional futures markets do not have.

This is what fragmentation looks like at scale, before the all-asset expansion has fully started. Each new asset class moving onto perpetual rails is being born into the same structure. New perps inherit the non-fungibility problem from day one.

VI. The future of liquidity in this regime

For institutions, the converged-but-fragmented structure creates a problem traditional futures markets did not have. No single connection gives access to the full liquidity pool for any given exposure. Each venue is its own liquidity island, with its own contract specifications, margin requirements, and funding rate dynamics.

Two participant types benefit from this structure.

Arbitrageurs harvest persistent spreads between non-fungible perps on different venues. Funding rate differentials, with one venue running +0.04% per 8 hours while another shows +0.01%, generate market-neutral returns of several hundred basis points annualized for participants with the infrastructure to capture them.11

This is the same pattern that drove proprietary trading firms into US equity market structure after RegNMS in 2007. One important difference is worth flagging. RegNMS worked because it was a domestic regulatory framework imposed within a single jurisdiction. The fragmentation in crypto-native markets is global by construction, with venues domiciled across jurisdictions that have no shared regulatory framework and limited history of meaningful coordination. A RegNMS-style solution to crypto fragmentation would require cross-border regulatory cooperation that does not currently exist and shows little evidence of emerging. The market will solve fragmentation on its own, through arbitrageurs and brokers, rather than through harmonized rules.

Brokers benefit too. As venue count grows, the operational cost of maintaining direct connections rises sharply for institutions whose primary business is not trading infrastructure. A broker layer that aggregates access becomes structurally necessary. Most institutional flow will be intermediated this way, the way most equity flow today is intermediated by a handful of prime brokers.

The number of distinct venues each winning a different slice of the converged all-asset perpetual market. There is no single platform consolidating institutional flow across crypto perpetuals, tokenized equities, commodities, and FX derivatives. The structural endpoint resembles equity market structure circa 2010, not a single-venue future.

Capital efficiency is the structural pressure that compounds the broker thesis. In a fragmented multi-venue market, capital trapped on the wrong venue is capital not generating returns. An institution running long on one venue and short on another to capture a funding rate spread needs collateral posted on both venues simultaneously. Multiply that across 6 to 8 venues, multiple asset classes, and varying margin regimes, and the capital requirements compound quickly. The ability to net exposures across venues, post collateral once, and have it recognized everywhere becomes the single most valuable institutional feature in the converged market. Cross-margining, portfolio margin, and unified collateral pools are not nice-to-have features. They are structural prerequisites for institutional scale.

VII. What to watch

The market structure of the next decade will not be “crypto” or “TradFi.” It will be the structure crypto built, with global access, 24/7 trading, self-custody, instant settlement, and perpetual derivatives, applied to every asset class that can inherit those properties.

What is less clear is how the structural details resolve. Three questions matter most.

Which all-asset platforms emerge as category winners.

Hyperliquid leads in on-chain perpetual crypto and is moving into commodities. CME owns regulated US institutional crypto derivatives. Robinhood and Aster are pushing into tokenized equities from opposite ends. None of these venues compete directly today. They will.

Whether 24-hour equity trading gains real volume.

If tokenized equities provide a convenient wrapper for global continuous trading of US single names, and perpetuals make leverage and shorting symmetric in a way SSFs never achieved, the demand pattern that has driven the growth of single-name leveraged trading in crypto could play out for US equities in tokenized form.

The US regulatory trajectory.

Perpetuals are not currently available to US persons through most venues, but the CFTC has been actively engaged and several US-regulated platforms are preparing to launch through self-certification.12 When, not if, perpetuals become broadly accessible to US institutions, volume migration will be rapid.

The honest summary is that “how should an institution think about crypto market structure” is no longer a crypto-specific question. It is the same question as how institutions should think about the future structure of equities, commodities, FX, and credit. The format that started in crypto is becoming the format for everything. The institutions that recognize this early will build the infrastructure to operate inside it. The institutions that do not will find themselves adapting to a market structure they did not design.

Sources

1. CoinGecko, 2025 Annual Crypto Industry Report; CryptoQuant via Reuters.

2. TD Securities, Perpetual Futures: The Missing Link in Tokenized Equities.

3. CoinGecko, State of Crypto Perpetuals 2024 and 2025 Annual Report.

4. Real-World Assets in On-chain Finance Report (RedStone, Gauntlet, RWA.xyz, June 2025); Chainalysis (April 2026).

5. KuCoin News, citing Hyperliquid trading data, February 2026.

6. Binance announcements (January and April 2026); The Block; DL News.

7. OKX announcements (March 2026).

8. The Defiant, RWAs Became Wall Street’s Gateway to Crypto in 2025.

9. Sahoo, Single-stock futures: Evidence from the Indian securities market, ScienceDirect; Cogent Economics & Finance.

10. CoinGecko, State of Crypto Perpetuals 2024 and 2025 Annual Report.

11. Sei Network blog, citing funding rate arbitrage research.

12. Reuters via CP24, April 2026.